Lenders issued foreclosure notices for 62 high-risk loans in the commercial real estate sector for this year ending in October, double last year’s total and possibly the highest number ever, according to a WSJ analysis. Many of those foreclosures are from mezzanine loans, or high-risk property loans that allow for a shorter time to foreclosure and have higher interest rates, with the shorter time frame giving a more immediate pulse on the health of the sector and forecasting a possible wave of foreclosures in the future on more traditional loans.

“A lot of borrowers have basically said, ‘I can’t hold this asset any longer; I can’t keep putting money in,’” Terri Adler, managing partner at the law firm Adler & Stachenfeld, told the WSJ. “And the lenders have said, ‘OK, we’ll take it back.’”

Commercial real estate foreclosures, while still presently low, are a lagging indicator of the sector’s health, as there can be a gap of a few months to years between a default and a foreclosure on more traditional loans, according to the WSJ. The total dollar amount for mezzanine loan foreclosures, despite the increase, is not known as the loan type does not appear on property records due to its opaque nature.

'Delinquent commercial real estate loans at US banks have hit their highest level in a decade, as higher interest rates, an uncertain economy and the rise of remote working pile pressure on building owners.' https://t.co/DXNOUAOJU3 pic.twitter.com/YtpawnQLQl

— Jesse Felder (@jessefelder) November 9, 2023

Regulators have forced bigger banks to be more cautious since the 2008 financial crisis, where a bubble in the real estate market burst after banks issued an exceptional number of risky loans, leading to the recent rise in mezzanine loans, which avoid this regulation to fill that demand for riskier loans, according to the WSJ. Smaller banks, debt funds or nonbank lenders fill this gap with mezzanine loans that entice lenders with interest rates often above 10%.

Mortgage rates reached a recent peak near the end of October at 7.9%, the highest point since September 2000. Residential home affordability has also suffered, with the average American only being able to afford a 30-year mortgage on a $356,273 house as opposed to that same family being able to afford a $737,392 house in December 2020.

Interest rates across all forms of debt are facing upward pressure from the Federal Reserve’s federal funds rate hikes. The rate has been put in a range of 5.25% and 5.50%, a 22-year high, following a series of 11 hikes in an effort to combat inflation, which peaked at 9.1% in June 2022.

Leave your thoughts on the Economic Collapse Substack.

All content created by the Daily Caller News Foundation, an independent and nonpartisan newswire service, is available without charge to any legitimate news publisher that can provide a large audience. All republished articles must include our logo, our reporter’s byline and their DCNF affiliation. For any questions about our guidelines or partnering with us, please contact [email protected].

]]>David Webb, a former hedge fund manager, and Wall Street insider, has blown the lid off a diabolical plan more than 50 years in the making in a shocking new book.

He calls it The Great Taking. I consider it an urgent must-read (available for free here).

Here’s the synopsis (emphasis mine):

It is about the taking of collateral (all of it), the end game of the current globally synchronous debt accumulation super cycle.

This scheme is being executed by long-planned, intelligent design, the audacity and scope of which is difficult for the mind to encompass.

Included are all financial assets and bank deposits, all stocks and bonds; and hence, all underlying property of all public corporations, including all inventories, plant and equipment; land, mineral deposits, inventions and intellectual property.

Privately owned personal and real property financed with any amount of debt will likewise be taken, as will the assets of privately owned businesses which have been financed with debt.

If even partially successful, this will be the greatest conquest and subjugation in world history.

Private, closely held control of ALL central banks, and hence of all money creation, has allowed a very few people to control all political parties and governments; the intelligence agencies and their myriad front organizations; the armed forces and the police; the major corporations and, of course, the media. These very few people are the prime movers. Their plans are executed over decades. Their control is opaque.

To be clear, it is these very few people, who are hidden from you, who are behind this scheme to confiscate all assets, who are waging a hybrid war against humanity.

Webb shows how the dark forces behind central banking have spent the last 50 years meticulously putting the legal structures in place worldwide to sever property rights for securities.

Gone are the days of physical paper share certificates and bearer securities, where you had control and ownership of the asset.

Today, your control and ownership have become increasingly distant as stocks, bonds, and other investments have been centralized away from account holders and rehypothecated—a slimy practice where financial institutions reuse an account holder’s asset for their own purposes, creating multiple claims on the same asset.

Contrary to what most brokerage account holders believe, they only have the appearance of ownership. If their broker goes bust, the stocks and bonds they think they own will be used to satisfy the other more senior creditors of their broker.

Webb shows how, during the 2008 financial crisis, a small broker in Florida went bankrupt. Instead of sending the clients’ securities to another broker, as had traditionally been the case, they were swept up by the bankruptcy receiver. But it’s not just some isolated small broker.

The bankruptcy of Lehman Brothers set the case law precedent for secured creditors to take client assets in the case of insolvency.

The most senior secured creditors are the most powerful financial institutions closest to the central banks—JP Morgan, BlackRock, Goldman Sachs, etc.

The net effect of The Great Taking will be the biggest centralization of money and power in history as they take everyone’s securities during a future crisis.

Though it’s not just securities, they will also take ANY asset financed by debt—like real estate, cars, and small businesses—as people become unable to service their debts. Webb provides all the details and proof in his book.

Here’s the bottom line. The most powerful people in the world have succeeded in subverting the property rights of securities and ensnaring most of the world with debt. The trap has been set, and the legal plumbing is in place.

All that is needed is a big crisis that will cause a tidal wave of bankruptcies, and the hidden forces behind the world’s central banks will be able to take everyone’s stocks, bonds, and any property financed by debt.

All the assets people think they own in brokerage accounts, bank accounts, pensions, and other financial accounts could vanish overnight.

Webb says, “There will be a game of musical chairs. When the music stops, you will not have a seat. It is designed to work that way.”

The Coming Collapse Is by Design

Webb makes a compelling case that the next financial crisis won’t be an accident; the global elite are making it happen to proceed with The Great Taking.

In short, it’s not plausible that such an intelligent, deliberate plan executed with persistence for more than 50 years could happen by accident.

Further, the forces behind central banking and (fake) money creation undoubtedly understand the dynamics of the boom-bust cycle they create by expanding and contracting the money supply.

They know the Everything Bubble they created will lead to a massive bust. That’s when they will execute The Great Taking. Further, consumer debt is at record highs.

After many years of being encouraged to go deeply into debt, many Americans have reached their maximum debt saturation. They will be ripe for the picking.

As Webb explains:

“Debt is not a real thing. It is an invention, a construct designed to take real things.

The bottom line is that debt has for centuries had the function of dispossessing, of taking away property, capital and investments from someone.”

What You Can Do About It

Nobody knows the future or how The Great Taking will play out. The best you can do is to make yourself a hard target and not be among the low-hanging fruit.

You can do that by being debt-free and owning unencumbered assets within your direct control.

You don’t want to own something that is simultaneously someone else’s liability. That’s because the legal structures are already in place to take it from you during the next crisis.

Crucially, this includes fiat currency in bank accounts. Remember, fiat currency is the unbacked liability of a bankrupt government.

Further, once you deposit currency into a bank, it is no longer yours. Technically and legally, it is the bank’s property, and what you own instead is an unsecured liability of the bank. As The Great Taking unfolds, you won’t want to be on the other end of liabilities or IOUs.

Three solutions stand out to me.

First, physical gold and silver bullion coins in your possession are an excellent option. The best way is to purchase widely recognized bullion coins, like the Canadian Maple Leaf or the American Eagle. Also, never put precious metals in a bank’s safe deposit box. They will be among the first targets when The Great Taking unfolds.

Second, real estate, businesses, and other property owned outright with no debt or any other competing claims attached to them.

Third, there is Bitcoin. Bitcoin is a digital bearer instrument. A bearer instrument gives whoever has it in their possession ownership of it, like the physical paper share certificates and bearer securities of the past.

When you properly hold Bitcoin, you own an asset that is NOT someone else’s liability and remains totally under your control.

Bitcoin has the potential to separate money from the state and give monetary sovereignty to the individual by rendering central banks obsolete—along with their confetti currencies.

That’s why Bitcoin is like kryptonite to the dark forces behind The Great Taking.

I’ve just released an urgent PDF report revealing three crucial Bitcoin techniques to ensure you avoid the most common—sometimes fatal—mistakes. Check it out as soon as possible because it could soon be too late to take action. Click here to get it now.

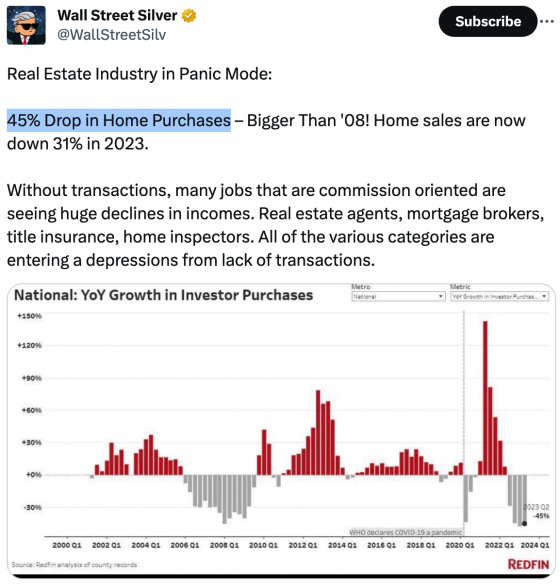

]]>The distortions we are witnessing in the housing market this year haven’t happened in more than a decade. For instance, the latest numbers show that year-over-year sales of existing homes have fallen to a level that we’ve not seen in 13 years. Adding to the bleak outlook, investor purchases sunk by 45% over the past twelve months, data from real estate brokerage Redfin reveals.

Economists at Fannie Mae are warning that this may be the beginning of a prolonged freeze. The experts projected in a revised forecast that stagnation in the housing market could last into 2024, whether economic conditions improve or worsen. “Regardless of whether a soft landing is achieved over the coming year, we expect existing home sales to stay subdued and within a tight range,” they wrote.

Moreover, when home sales crash, everybody who works in the real estate industry suffers. The situation is also getting dire on the commercial real estate side. he Wall Street Journal recently published an article entitled “Real-Estate Doom Loop Threatens America’s Banks”, and that headline is actually not an exaggeration of the current state of affairs. Commercial real estate prices are plunging all over the nation, and major U.S. banks have trillions of dollars of exposure.

This shows that many of our financial institutions are at serious risk of experiencing widespread losses. If the Federal Reserve were to stop raising rates immediately, that would help. But officials continue to insist that rates are going to go even higher, and that is going to escalate this crisis into a full-blown real estate apocalypse.

Instead of realizing the damage that has been done and starting to fix the problem, Federal Reserve Chairman Jerome Powell warned on Friday that additional rate increases might be required to put inflation on a convincing path to the central bank’s two percent target.

We have got a major crisis on our hands, and it is not going to go away any time soon. The administration told us over and over again that “Bidenomics” was working, but that’s not what we’re seeing on real terms. If this feels familiar, it’s because it is. And we know how ugly things have gotten the last time around. The housing bubble burst has already begun, and a historic crash in property values is coming next. We have now entered the very early chapters of a full-blown economic nightmare.

Conditions are going to get a whole lot worse for the real estate industry. And things are going to get a whole lot worse for the economy as a whole. So we truly hope that you have been getting prepared for what is ahead because most Americans are going to get completely blind-sided by the disaster we’re about to face.

Article and video from Epic Economist.

]]>When home sales crash, everybody that works in the real estate industry suffers.

And it turns out that home purchases by investors are falling at an even faster rate. Wall Street Silver posted the following to Twitter earlier this week…

I was stunned when I first saw that, but I also knew that I had to confirm if this was true or not.

And I discovered that it is true…

45%

That’s how much investor purchases of homes have fallen since last year, as of the second quarter, according to data from Redfin, as homebuying looks less profitable than during the pandemic housing boom.

Investors, just like private buyers, think it’s a bad time to buy a home.

We have got a major crisis on our hands, and it is not going to go away any time soon.

Things are even worse on the commercial real estate side.

The Wall Street Journal just published an article entitled “Real-Estate Doom Loop Threatens America’s Banks”, and that headline does not exaggerate the current state of affairs at all.

Commercial real estate prices are plummeting all over the nation, and our banks have trillions of dollars of exposure…

The WSJ analysis put total bank exposure to commercial real estate at $3.6 trillion, which it estimates is 20 percent of their deposits. Holdings of CMBS and loans to nonbank lenders accounted for $623 billion of that total at the end of last year.

In the past decade, regional banks went to town on commercial loans, never expecting how quickly the tide would turn against them. Today, losses on loans are leading banks to cut back on lending, furthering the drop in property prices and more lender losses — in other words, a doom loop.

Banks are already pulling back. Debt origination fell by 52 percent for the second quarter year-over-year, according to Newmark; lending volume among banks fell by 48 percent. M&T Bank said it would reduce commercial lending as nearly 1 in 5 of its loans to office landlords was in trouble.

So many of our financial institutions are going to be in very serious trouble because of this.

If the Federal Reserve were to push interest rates all the way to the floor immediately, that would help.

But instead, Fed officials continue to insist that rates are going to go even higher, and that is going to escalate this crisis into a full-blown real estate apocalypse.

And higher rates will also do an incredible amount of damage throughout the rest of the economy as well. This is a point that the Shark Tank’s Kevin O’Leary made very well during a recent interview with Fox Business…

In a recent interview on Fox Business, Kevin O’Leary, the “Shark Tank” investor slammed so-called “Bidenomics” for leaving small businesses behind. He warned that chaos is about to kick off for the “little guy”, which are the 33.2 million small businesses in America, due to the Federal Reserve’s aggressive rate hikes.

“They’re struggling because the Fed has raised rates up to 5.5% in a matter of months,” O’Leary said. “You’re going to hear a lot of people crying about this in the next few months because they can’t borrow anything anymore and they can’t run their businesses.”

He is right.

Small and mid-size businesses all over America are really struggling right now.

Economic activity is slowing down all around us, and they are starting to lay off workers.

In fact, in just the past two months the U.S. has lost a whopping 670,000 full-time jobs…

Well, one look at this month’s adjustment and it’s literally a shocker: you will not hear anyone from the Biden admin or associated economist cheerleaders mention this, but the BLS reported that in August the number of full-time jobs dropped again, sliding by 85K to 134.2 million, and followed the whopping 585K plunge in July which brings the two-month total drop in full-time jobs to a whopping 670K, the biggest 2-month plunge since the covid lockdowns in early 2020 when 12.5 million full-time jobs were lost in one month!

When the official numbers that the government gives us start looking this bad, you know that the hour is late.

And the job cuts just keep on coming. On Wednesday, we learned that Roku will be conducting a third round of layoffs…

Video streaming company Roku shares spiked Wednesday after it announced plans to lay off more than 300 people, or about 10% of its workforce, and pull certain content from its streaming platform to ease operating expenses.

This is the third round of layoffs from Roku in recent months after the company let go of about 400 employees total between November and March. The company had roughly 3,600 full-time employees across 14 countries at the end of last year, according to its annual report.

I actually really like Roku, and so I hope they can turn things around.

But the reality of the matter is that everyone is going to have to deal with the very hard times that are now upon us.

Hordes of middle class Americans are being pushed into poverty, and hordes of impoverished Americans are being forced into the streets.

So far this year, we have actually seen “the biggest ever spike in homeless people living on the streets”…

The United States has seen the biggest ever spike in homeless people living on the streets – as preliminary figures showed a record 11 percent increase in one year.

There are nearly 600,000 rough sleepers across cities and towns in America, and the jump from 2022 to 2023 so far is the highest since the government started tracking the data in 2007, according to the WSJ.

Places like Oakland and San Francisco in California have become hotbeds for homelessness, as people living on the streets are like ‘drug tourists’ who arrive to have easy access to narcotics.

But this isn’t supposed to be happening.

The Biden administration told us over and over again that “Bidenomics” was working. Of course the truth is that we have now entered the very early chapters of a full-blown economic nightmare.

Things are going to get a whole lot worse for the real estate industry. And things are going to get a whole lot worse for the economy as a whole.

So I hope that you have been getting prepared for what is ahead, because most Americans are going to get completely blind-sided by what is coming.

Sound off about this story on our Economic Collapse Substack.

Michael’s new book entitled “End Times” is now available in paperback and for the Kindle on Amazon.com, and you can check out his new Substack newsletter right here. Article cross-posted from The Economic Collapse Blog.

]]>In fact, in overvalued markets, homeowners may see the value of their properties drop by half before we enter 2024, according to experts’ estimates. This can translate into a six-digit loss in home equity in just one year. Conditions are getting eerily similar to the ones that led to the 2008 financial crisis, a famous Big Short investor says. In other words, now we all must keep a close eye the on the reg flags that indicate we’re heading into another disaster.

At this point, approximately 37 of the 50 largest markets in the country have already reported double-digit price drops, with homes in some markets falling by up to 25% from their 2022 peak, according to NAR chief economist, Lawrence Yun. During an interview with Insider, the expert revealed that home prices will fall by half in overvalued markets, and that’s especially true for metros in the West, where he is forecasting 0% home-price growth in 2023.

Goldman Sachs analysts wrote that “overheated housing markets in the Southwest and Pacific coast, such as San Jose MSA, Austin MSA, Phoenix MSA, and San Diego MSA will likely grapple with another decline of over 25 percent, presenting a localized risk of higher delinquencies for mortgages originated in 2022 or late 2021.”

A notorious Big Short investor says that once again conditions are pointing to a financial nightmare. Dave Burt, CEO of investment research firm DeltaTerra Capital which helps clients manage risks, was one of the few experts who recognized the housing market was falling apart in 2007.

“I’m always on the lookout for big systemic issues and there are a few reasons for that,” Burt told CNBC. The correction that is already in motion will be “very, very damaging within those exposed communities,” Burt warned. Concerns over a housing crash are also panicking investors like Jeff Greene, who made a lot of his wealth during the 2008 recession and is warning about a destructive period across the entire real estate market.

Jeffrey Roach, chief economist for LPL Financial in Charlotte, North Carolina, said in a statement that the current Fed outlook is reminiscent of 2007 before the housing market crashed. “This current environment could be eerily similar to early 2007 when the Fed held a tightening bias on rates as they believed the housing market was stabilizing, the economy would continue to expand, and inflation risks remained,” Roach said. “Clearly, those expectations were not met since we know what happened in later quarters. Investors should anticipate some volatility during these months where the economic outlook remains cloudy.”

Sadly, even though the drop in prices may be good news for aspiring homebuyers hoping to catch a break, the crash could ultimately wipe out $100,000 of the value of the average home, NAR estimates. This would leave many families with negative home equity, and a mortgage crisis could break out, plunging us into the worst financial crisis in modern times. The red flags are many, and we all should stay alert and carefully watch the new developments of this crisis.

Article and video via Epic Economist.

]]>No, instead they just created an even bigger housing bubble. Now that housing bubble is beginning to burst, and that is going to have very serious implications for all of us.

One thing that we learned during the Great Recession is that home values really matter.

When home values get low enough, many borrowers simply decide to walk away from their mortgages, and so the fact that U.S. home values have plummeted by 108.4 billion dollars should deeply alarm all of us…

Homeowners are sitting on a negative equity timebomb after losing $108.4 billion on their property values this year, experts say.

The average borrower saw their home equity plummet by $5,400 in the first quarter of 2023 compared to last year – with households in Washington, California and Utah worst affected.

The west coast is being hit particularly hard. For example, home values in Washington state have dropped by an average of more than $74,000 over the past year…

The cooling housing market is stripping more equity from homeowners in Washington than in any other state in the country.

On average over the last year, Washington homeowners lost about $74,300 in equity, a measure of the difference between how much a home is worth and how much the owner owes on the mortgage, according to the real estate data company CoreLogic. That 18% decline marked the largest drop in the country from the first quarter of last year to the first quarter of 2023.

Some homeowners in Washington state that bought their homes at the peak of the market now have mortgages that are underwater.

And according to an expert that was interviewed by the Daily Mail, this is starting to happen in certain areas all over the nation…

Zackary Smigel, founder of Real Estate License Wizard, told DailyMail.com: ‘The decline in property values across the US is posing significant challenges to homeowners – and it’s becoming a bigger issue in the real estate sector.

‘We are indeed witnessing some worrying signs of negative equity, especially in certain regions.’

The good news is that this is not happening everywhere.

So many people have been relocating to Florida that home prices have actually gone up substantially in that state. If you want to get an idea of what has been happening where you live, you can check out this map.

Moving forward, I think that home prices will not move uniformly.

In major cities and in blue states, I believe that home prices will tend to fall. In rural areas and in red states, I believe that home prices will be more stable.

Meanwhile, many commercial real estate loans all over the U.S. are already deeply underwater, and we are starting to see delinquency rates rise at a startling pace.

If you doubt this, just check out these numbers which come from Wolf Richter…

After blowing through the pandemic with no more than a squiggle, the delinquency rate of Commercial Mortgage-Backed Securities (CMBS) backed by office properties jumped to 4.5% by loan balance in June, up from 1.6% just six months ago in December 2022, according to Trepp, which tracks and analyses CMBS.

Office mortgages that had been packaged into CMBS went through a horrendous default cycle following the Financial Crisis, with the delinquency rate topping out at over 10% in 2012/2013.

But this current six-month 2.9-percentage-point spike from 1.6% to 4.5% is the fastest six-month spike in Trepp’s data going back to 2000.

We are still in the early chapters of this crisis, but it is definitely eerily similar to what we witnessed in 2008.

Corporate bankruptcies are also surging.

In fact, it is being reported that they were up 93 percent during the first six months of this year compared to the same time period of time in 2022…

In the first six months of 2023, there were 340 corporate bankruptcies, topping every other comparable span in 13 years, according to S&P Global Market Intelligence. This is up 93 percent from the same time a year ago and higher than in 2020, when there was a spike during the early days of the coronavirus pandemic.

When we keep getting numbers like this, I honestly don’t know how anyone can claim that the U.S. economy is moving in the right direction. There are so many signs of trouble all around us. For example, the number of searches for “pawn shop near me” just soared to an all-time record high…

Cash-strapped Americans are panic-searching “pawn shop near me.” The search trend spiked to a record high at the start of July and is an ominous sign the consumer might be pawning items or selling things that were possibly bought during the Covid boom to raise quick money amid the worst inflation storm in a generation.

Needless to say, people don’t pawn their possessions when they are doing well.

Searches for the phrase “is dumpster diving illegal” also just reached an all-time record high.

All over the nation, people are literally rummaging through dumpsters behind grocery stores because food has become so oppressively expensive. But don’t worry. Joe Biden says that everything is going to be okay.

If you have been following my articles on a regular basis, nothing that I have shared in this piece should come as a surprise to you. It was clear way in advance that the economy was heading into enormous trouble, and the long-term outlook is exceedingly bleak.

But that doesn’t mean that you should crawl into a corner and cry like a baby because things are going to get so bad. It is when times are the darkest that the greatest courage is needed.

You were born for such a time as this, and you can make a difference even in the midst of all the chaos that is starting to erupt all around us.

Michael’s new book entitled “End Times” is now available in paperback and for the Kindle on Amazon.com, and you can check out his new Substack newsletter right here.

Article cross-posted from The Economic Collapse Blog.

]]>The chart, which was withdrawn after widespread protest, sought to identify the characteristics needed to build not only an economy but civilization itself with a racist culture. Thus, the kind of lifestyle and values that might culminate in someone having high credit scores and saving up for a significant down payment for a house were something not to be emulated or praised, but rather to be called out and declared shameful.

Although the chart no longer is found on the Smithsonian website, the mentality that created it lives on in the policies of the Biden administration. To show its commitment to equity—equal outcomes—the Federal Housing Finance Agency (FHFA) implemented a new policy on May 1, 2023, that punishes homebuyers with high credit scores who can put down at least 15–20 percent on a mortgage by making them pay higher interest rates and extra fees. Declares a Wall Street Journal editorial:

According to calculations by Evercore ISI, buyers with strong credit scores between 720 and 739 who make 15%–20% down payments will see their rates increase by 0.750%. Borrowers who put down 20%–25% will see rates increase by 0.500%.

The winners are borrowers with weak credit scores—that is, riskier borrowers. Under current FHFA policy, a borrower with a weak credit score below 620, who is borrowing more than 95% of the value of their home, pays 3.750%. Under Ms. Thompson’s new plan, those borrowers will see their fees decrease by 1.750%.

Not surprisingly, commentators like James Bovard have rightly attacked this policy as one that imposes perverse incentives, turning the rewards for creditworthiness upside down. Bovard writes:

Starting May 1, The Post exposed last week, a Biden administration decree will require adjusting mortgage calculations to penalize homebuyers with a FICO credit score of 680 and above—almost two-thirds of the population.

This levy will be used to reduce costs for people with low credit scores—i.e., risky borrowers more likely to default on mortgages.

However, this is not merely another version of the Law of Unintended Consequences, in which well-meaning government officials implement a policy without looking at the so-called bigger picture.

The consequences here are intended. The Biden administration officials know full well the implications of this new policy and is sending the message that the notion of creditworthiness itself is implicitly racist.

As Newsweek points out, the racial gaps in home ownership and credit scores are significant:

Only about 25 percent of homebuyers with Federal Housing Administration loans are people of color, according to the White House. Black and Hispanic people, on average, have fewer savings to use as a down payment on a home and tend to have lower credit scores, according to David Stevens, former CEO of the Mortgage Bankers Association (MBA) and a former FHA commissioner during the Obama administration. The current policy is being rolled out by the FHFA.

He told Newsweek that this can be attributed to factors like distrust in the banking system or being a first-generation American. He added that low credit scores can be a significant barrier to homeownership.

But in order for the FHFA to close the gap by bringing down LLPAs [loan-level price adjustments] for those borrowers, the agency will compensate for the reduction in borrowing fees by raising the LLPAs of borrowers with higher credit scores, who tend to be white.

The average credit score in white communities was 727 in 2021, compared with 667 in Hispanic communities and 627 in Black communities, according to data analyzed by FinMasters, a personal finance blog.

Not surprisingly, the Biden administration blames the homeownership gap on racism, so its proclivity is to punish the people who saved their income and engaged in forward-looking behavior, something the Smithsonian condemned as a product of “whiteness.” However, as Bovard points out, black homeownership rates relative to white rates are lower today than they were more than fifty years ago: “Federal Housing Finance Agency Director Sandra Thompson testified to Congress last year that the racial homeownership gap ‘is higher today than when the Fair Housing Act [of 1968] was passed.’”

That is hardly insignificant. In 1968, the United States was just beginning to shed Jim Crow laws, and prospective black homeowners had far fewer financing opportunities than they do today. Furthermore, homebuyers were expected to put at least 20 percent down, with only some exceptions, so one might consider lending policies at that time to have been far less friendly to black borrowers than they are today.

Furthermore, the Bill Clinton, George W. Bush, and Barack Obama administrations had policies explicitly aimed at increasing homeownership among blacks and other minority groups. Bush claimed his administration had put a record number of black Americans in their own homes by helping to provide down payments and lowering interest rates, among other policies.

Andrew Cuomo, the Clinton administration’s housing and urban development secretary, declared that the homeowning gap between blacks and whites was due to discrimination and ordered mortgage lenders to lower lending barriers for black households. Cuomo wrote:

The American Dream of homeownership is not reserved for whites. We will not tolerate a continued homeownership gap as wide as the Grand Canyon that divides Americans into two societies, separate and unequal. Eliminating housing and lending discrimination is vital to making the opportunity for homeownership a reality for all Americans.

Of course, the Bush administration’s all-out push to increase black and Hispanic homeownership rates had its own unhappy ending: the 2008 financial meltdown. All the Bush administration’s efforts to increase minority home ownership blew up as home prices plunged and many homeowners defaulted on their mortgages and lost their homes. Writes Bovard: “Thanks to the housing crash, the median net worth for Hispanic households declined by 66 percent between 2005 and 2009 and the median net worth of black households declined by 53 percent.”

Moreover, in a 2004 article in Barron’s, Bovard warned that the Bush housing policies were going to have an unhappy ending:

One of the proudest elements of President Bush’s “compassionate conservative” agenda has been government financial support to home buyers for down payments. Bush is determined to end the bias against people who want to buy a home but don’t have any money. But he is exposing taxpayers to tens of billions of dollars of possible losses, luring thousands of moderate-income families into bankruptcy, and risking the destruction of entire neighborhoods.

Bovard’s words were prophetic. But at least Bush didn’t blame borrowers with high credit scores and large down payments for the racial housing gaps.

The Biden administration, on the other hand, has expanded the definition of “intersectionality” to include the claim that whites (along with non-whites who have high credit scores) are to blame for minorities’ low credit scores and shakier finances. The Biden administration’s policies continue what Bovard called “wrecking ball benevolence.” Former federal Judge Janice Rogers Brown concurred, writing: “Whether the road was paved with good intentions or greased by greed and indifference, affordable housing turned out to be the path to perdition for the U.S. mortgage market.”

Economically, none of this makes sense, but one must understand that the Biden administration is not looking to promote working markets in housing. Instead, it is claiming that the only cause of the gap in homeownership between blacks and whites is white racism and that the government must engage in extraordinary means to eliminate this gap, even if this requires turning economic logic upside down.

One does not have to be a seer or have a doctorate in economics to know that this latest iteration of federal housing policy will end in failure just like all the other housing initiatives for minorities. But don’t blame the Law of Unintended Consequences. This new policy is deliberate, and when it fails (as it surely will), look for Biden or whoever else is in the White House to call for even more drastic measures.

About the Author

William L. Anderson is Senior Editor at the Mises Institute and professor emeritus of economics at Frostburg State University in Frostburg, Maryland.

Article cross-posted from Mises.

]]>But did you know that there was another housing crash exactly 14 years before the one that we witnessed in 2008?

In 1994, surging mortgage rates caused new home sales to plunge dramatically…

The average 30-year fixed mortgage rate increased by around 2 percentage points in 1994, ending the year north of 9%. New home sales slumped. In December 1993, the seasonally adjusted annual rate of new single-family-home sales was 812,000. A year later, in December 1994, it had fallen over 20% to 629,000.

That kind of sounds like what we are experiencing right now.

And if you go back 14 years before that, you will find another housing crash.

The U.S. housing market was booming in 1978 under Jimmy Carter, but higher interest rates caused things to cool off in 1979, and then in 1980 home sales really began to tumble. Ultimately, the level of existing home sales tumbled by about 50 percent over a four year period…

From the peak of 4 million existing-home sales in 1978, there was -50% drop in home sales over the next four years, so that by 1982 only 2 million homes were sold (data here, Table 7). It took almost two decades, or until 1996, before home sales exceeded the 1978 level of 4 million units.

The Federal Reserve knows what has happened in the past when they have aggressively hiked rates.

But they are doing it again anyway.

So here we are 14 years after the last housing crash, and it is starting to happen again. We just learned that sales of new single-family homes were about 30 percent lower this July than they were last July…

The plunge in home sales is just stunning. Sales of new single-family houses collapsed by 12.6% in July from the already beaten-down levels in June, and by nearly 30% from July last year, to a seasonally adjusted annual rate of 511,000 houses, the lowest since January 2016, and well below the lockdown lows, according to data from the Census Bureau today.

Those numbers are absolutely horrible, and every region of the country is getting monkey-hammered…

- Northeast: -37%

- West: -50%

- Midwest: -23%

- South: -21%

Sales of new single-family homes have now dropped for six of the last seven months.

That is clearly a trend.

Of course sales of previously owned homes have been falling quite rapidly as well…

Sales of previously owned homes fell nearly 6% in July compared with June, according to a monthly report from the National Association of Realtors.

The sales count declined to a seasonally adjusted annualized rate of 4.81 million units, the group added. It is the slowest sales pace since November 2015, with the exception of a brief plunge at the beginning of the Covid pandemic.

Sales dropped about 20% from the same month a year ago.

They are calling this a “housing recession”, but that isn’t what we are actually facing.

The truth is that we are in the early stages of another full-blown housing crash.

Just like we experienced in 2008. Just like we experienced in 1994. Just like we experienced in 1980.

Things are particularly bad in the markets that were once the hottest.

For example, just check out what has been going on in Boise, Idaho…

Nearly 70% of home sellers in Boise, Idaho cut the asking price on their house in July, Redfin reports; a remarkable turn for the once-hot real estate market.

Nationally, 32 percent of all home sellers cut their asking price last month.

Needless to say, prices are still way too high and they are likely to come down a lot more in the months ahead.

If you bought a house near the peak of the market, I really feel sorry for you.

Lots of people locked in mortgages at vastly elevated prices.

And now a lot of those same people are deeply regretting those decisions…

As the U.S. housing market cools, feverish competition for homes in the past couple of years has left 72% having regrets about their home purchases, according to a recent survey from Clever Real Estate.

The number-one reason for the buyer’s remorse: 30% of respondents said they spent too much money.

The exact same thing happened last time around too.

We never seem to learn from our mistakes, and now the stage is set for what could be the biggest housing crash of them all. We shall see what the Federal Reserve chooses to do.

If they stop raising rates, that will help. But if they decide to keep aggressively hiking rates, that will be absolutely catastrophic for the housing industry.

I have been warning that this sort of thing was coming for a long time, and now it is here. If you are looking to sell a home, try to do it as quickly as you can.

Because prices are going to continue to fall all over the nation, and it won’t be too long before vast numbers of homeowners are underwater on their mortgages.

***It is finally here! Michael’s new book entitled “7 Year Apocalypse” is now available in paperback and for the Kindle on Amazon.***

About the Author: My name is Michael and my brand new book entitled “7 Year Apocalypse” is now available on Amazon.com. In addition to my new book I have written five other books that are available on Amazon.com including “Lost Prophecies Of The Future Of America”, “The Beginning Of The End”, “Get Prepared Now”, and “Living A Life That Really Matters”. (#CommissionsEarned) When you purchase any of these books you help to support the work that I am doing, and one way that you can really help is by sending digital copies as gifts through Amazon to family and friends. Time is short, and I need help getting these warnings into the hands of as many people as possible.

I have published thousands of articles on The Economic Collapse Blog, End Of The American Dream and The Most Important News, and the articles that I publish on those sites are republished on dozens of other prominent websites all over the globe. I always freely and happily allow others to republish my articles on their own websites, but I also ask that they include this “About the Author” section with each article. The material contained in this article is for general information purposes only, and readers should consult licensed professionals before making any legal, business, financial or health decisions.

I encourage you to follow me on social media on Facebook and Twitter, and any way that you can share these articles with others is a great help. These are such troubled times, and people need hope. John 3:16 tells us about the hope that God has given us through Jesus Christ: “For God so loved the world, that he gave his only begotten Son, that whosoever believeth in him should not perish, but have everlasting life.” If you have not already done so, I strongly urge you to ask Jesus to be your Lord and Savior today.

Article cross-posted from The Economic Collapse Blog.

]]>Meanwhile, the National Association of Home Builders’ Housing Market Index, a measure of homebuilder sentiment, fell again in July, coming in at 55 versus 67 in June. That is the seventh consecutive drop and the second-largest monthly decline in the index’s history, putting the result at the lowest reading since May 2020. The index is down sharply from recent highs of 84 in December 2021 and 90 in November 2020 (see first chart).

According to the report, “Builder confidence plunged in July as high inflation and increased interest rates stalled the housing market by dramatically slowing sales and buyer traffic.” The report adds, “In another sign of a softening market, 13% of builders in the HMI survey reported reducing home prices in the past month to bolster sales and/or limit cancellations.”

All three components of the Housing Market Index fell again in July. The expected single-family sales index dropped to 50 from 61 in the prior month, the current single-family sales index was down to 64 from 76 in June, and the traffic of prospective buyers index sank again, hitting 37 from 48 in the prior month.

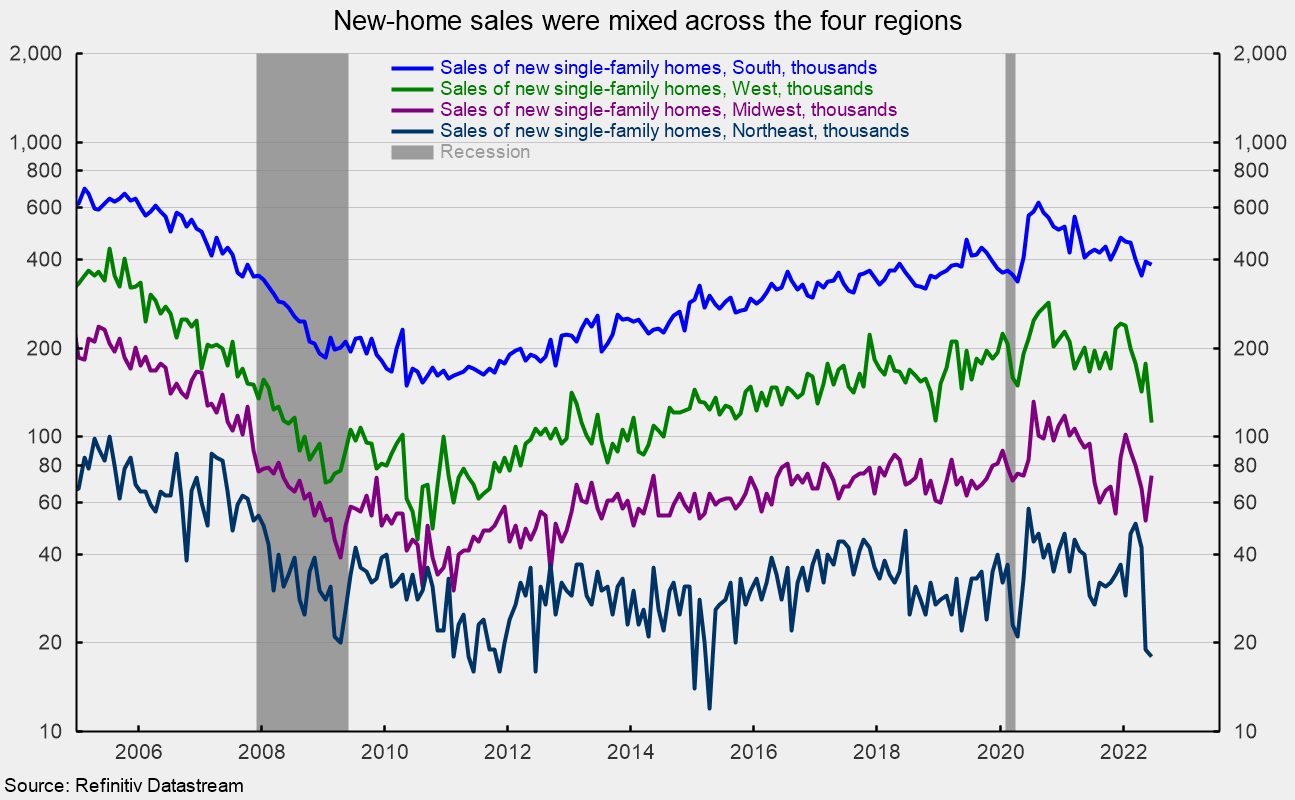

Sales of new single-family homes were down in three of the country’s four regions in June. Sales in the South, the largest by volume, fell 2.0 percent, while sales in the Northeast, the smallest region by volume, fell 5.3 percent, and sales in the West decreased 36.7 percent. Sales in the Midwest jumped 42.3 percent for the month. Over the last 12 months, sales were down across all four regions, led by a 37.9 percent fall in the Northeast, followed by a 32.9 percent drop in the West, a 22.1 percent decrease in the Midwest, and an 8.7 percent retreat in the South (see second chart).

The median sales price of a new single-family home was $402,400 (see third chart), down from $444,500 in May and a record high $457,000 in April (not seasonally adjusted). Meanwhile, 30-year fixed rate mortgages were 5.51 percent in late July, up sharply from a low of 2.65 percent in January 2021. The combination of high prices and rising mortgage rates is reducing affordability and squeezing some buyers out of the market.

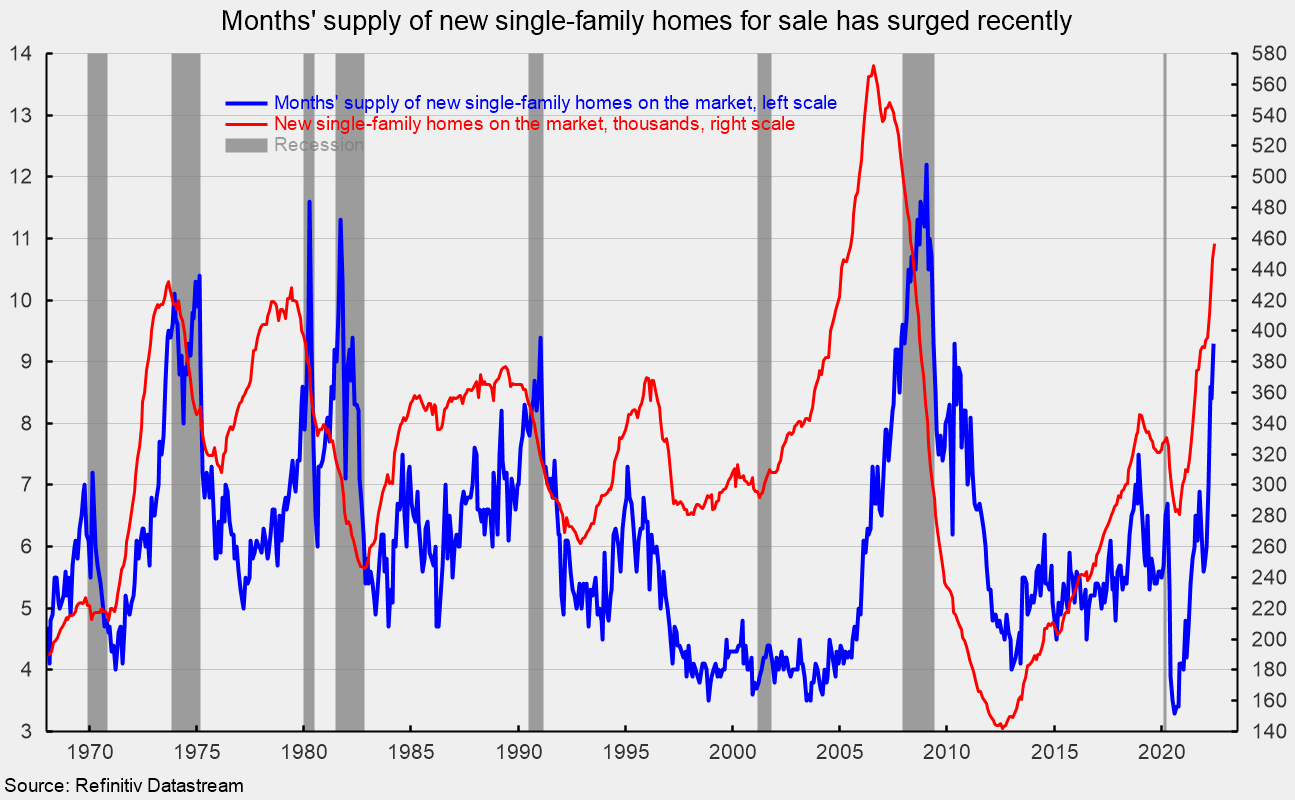

The total inventory of new single-family homes for sale rose 2.2 percent to 457,000 in June, the highest since April 2008. That puts the months’ supply (inventory times 12 divided by the annual selling rate) at 9.3, up 10.7 percent from May, 60.3 percent above the year-ago level, and the highest since May 2010. The months’ supply is very high by historical comparison (see fourth chart). The high level of prices, elevated months’ supply, and surge in mortgage rates should weigh on housing activity in the coming months and quarters. However, the median time on the market for a new home remained very low in June, coming in at 2.5 months versus 2.7 in May.

Image by F. Muhammad from Pixabay. Article cross-posted from AIER.

]]>- Investors’ participation in the housing market during the pandemic may have been instrumental in driving up prices and making it harder for the average American to achieve homeownership

- Investors with large portfolios nearly doubled their share of purchases from September 2020 to September 2021, reducing the supply of available housing — particularly in lower-priced markets — and driving up prices further

- Blackstone is the largest landlord in the U.S. as well as the largest real estate company worldwide, with a portfolio worth $325 billion

- BlackRock, one of the largest asset management firms, is another mega firm buying up U.S. houses; if trends continue, some believe Wall Street investors could accomplish feudalism in 15 years

- Aladdin, which stands for Asset, Liability, Debt, and Derivative Investment Network, is BlackRock’s technology platform, which controls $21 trillion of the global economy and has access to data on the global real estate market

Buying a home — often viewed as a cornerstone of the American dream — is getting harder to afford in the U.S. The reasons why are complex, a perfect storm of rising interest rates and high housing prices have priced many people out of the market.1 But there are other factors at play, including record-low inventory2 and competition from investors, who purchase homes in cash about 75% of the time.3

An influx of investors — including Wall Street — entered the housing market during the pandemic, drawn in by low mortgage rates, easy access to loans and enticing home appreciation.4

It’s now clear that not only did investors, including bigwigs like Blackstone and iBuyers — which make instant, cash offers online — dabble in the housing market during the pandemic, but their participation may have been instrumental in driving up prices and making it harder for the average American to achieve homeownership.5

Big Investors Doubled Their Share of Home Purchases

Investors range in size from small to large — spanning the space of mom-and-pop shops renting out a couple of vacation rentals to Wall Street giants with hundreds or thousands of units. Most investor home purchases (74%) in September 2021 were made by those with portfolios of less than 100 properties,6 but the gap is closing. Mega investors significantly expanded their scope in recent months, such that they’ve had a major impact on the market.

According to Daniel McCue, a senior research associate at the Harvard Joint Center for Housing Studies, “Adding to the pressure on prices, investors moved aggressively into the single-family market over the past year, buying up moderately priced homes either to convert to rental or upgrade for resale.”7 In “The State of the Nation’s Housing 2022,” a report by the Joint Center for Housing Studies of Harvard University, it’s further noted:8

“CoreLogic reports that the investor share of single-family homes sold in the first quarter of 2022 hit 28 percent, well above the 19 percent share a year earlier and the 16 percent share averaged in 2017–2019. Not surprisingly, investors focused on markets with rapid home price appreciation …”

However, investors with large portfolios are increasingly making their mark. They nearly doubled their share of purchases from September 2020 to September 2021, reducing the supply of available housing — particularly in lower-priced markets — and driving up prices further. According to the report:9

“Investors have moved rapidly into the single-family market since the pandemic began … Investors with large portfolios (at least 100 properties) drove much of this growth, nearly doubling their share of investor purchases from 14 percent in September 2020 to 26 percent in September 2021.

By buying up single-family homes, investors have reduced the already limited supply available to potential owner-occupants, particularly first-time and moderate-income buyers. Indeed, investors are more likely to target lower-priced properties.

In September 2021, investors bought 29 percent of the homes sold that were in the bottom third by metro area sales price, compared with 23 percent of homes sold in the top third. Investor-owned homes are typically converted from owner-occupied units to rentals or upgraded for resale at a higher price point.”

Blackstone Back in the Home-Buying Business

Blackstone, a giant private equity firm, is deeply entrenched in U.S. real estate. Blackstone is the largest landlord in the U.S. as well as the largest real estate company worldwide, with a portfolio worth $325 billion.10 In 2012, Blackstone founded Invitation Homes and spent billions buying foreclosures and distressed properties and turning them into single-family rental properties.

With about 80,000 homes in its portfolio, Invitation Homes has been criticized for evicting tenants, hiking rents, delaying repairs and charging excessive fees.11 At its peak, Blackstone was spending more than $100 million a week buying up properties.12

The company went public in 2017, raising more than $1.5 billion from its initial stock sale, but Blackstone sold its remaining shares of the company in 2019, earning about $7 billion.13,14 It re-entered the market during the pandemic, however, with a $300 million minority investment in Tricon Residential, which owns more than 30,000 single family and multifamily rental homes throughout the U.S. and Canada.15

In June 2021, Blackstone agreed to buy Home Partners of America, a company that rents single-family houses, and its more than 17,000 houses, for $6 billion.16

BlackRock Threatens Middle-Class Home Ownership

BlackRock, one of the largest asset management firms, is another mega firm buying up U.S. houses; they also control the media and Big Pharma, and have ties to Blackstone. Blackstone’s cofounder, billionaire Steve Schwarzman, said during an interview on Squawk Box that he and BlackRock founder and CEO Larry Fink started in business together.

“We put up the initial capital,” he said. BlackRock used to be called Blackstone Financial, but Fink went off on his own. Schwarzman said, “Larry and I were sitting down and he said, ‘What do you think sort of about having a family name with ‘black’ in it,’”17 and BlackRock was born.

In the first quarter of 2021, 15% of U.S. homes sold were purchased by corporate investors18 — competing with middle-class Americans for the homes. There’s really no competition, however, as the average American has virtually no chance of winning a home over an investment firm, which may pay 20% to 50% over asking price,19 in cash, sometimes scooping up entire neighborhoods at once so they can turn them into rentals.20

“Yield-chasing investors are snapping up single-family homes, competing with ordinary Americans and driving up prices,” The Wall Street Journal warned in a 2021 exposé.21 The question is: Why would institutional investors and BlackRock, which manages assets worth $5.7 trillion,22 be interested in overpaying for modest, single-family homes?

To understand the answer, you must look at BlackRock’s partners, which include the World Economic Forum (WEF),23 and their extreme political and financial clout. In a Twitter thread posted by user Culturalhusbandry, it’s noted:24,25

“Black Rock, Vanguard, and State Street control 20 trillion dollars worth of assets. Blackrock alone has a 10 billion a year surplus. That means with 5-20% down they can get mortgages on 130-170k homes every year. Or they can outright buy 30k homes per year. Just Blackrock.

… Now imagine every major institute doing this, because they are. It can be such a fast sweeping action that 30yrs may be overshooting it. They may accomplish feudalism in 15 years.”

If the average American is pushed out of the housing market, and most of the available housing is owned by investment groups and corporations, you become beholden to them as your landlord. This fulfills part of the Great Reset’s “new normal” dictum — the part where you will own nothing and be happy. This isn’t a conspiracy theory; it’s part of WEF’s 2030 agenda.26

BlackRock’s Aladdin ‘Owns Everything’

Aladdin, which stands for Asset, Liability, Debt, and Derivative Investment Network, is BlackRock’s technology platform, which controls $21 trillion of the global economy — that’s more than the $20 trillion GDP of the U.S., or the $15 trillion GDP of the E.U.27

To put this into perspective, if you were to collect every last cent from the world’s 7.6 billion people, you would amass about $5 trillion, which is considerably less than the $6.3 trillion in assets BlackRock is managing. As reported by The New Statesman:28

“The total value of assets under management by BlackRock is $6.3 trillion. But Aladdin also delivers risk analysis on the assets managed by its clients, which are valued at more than double that amount.

Overall, Aladdin has an effect on the management of around ten per cent of the world’s financial assets, or around $20 trillion. Over 25 years, it has grown into a system that is directly or indirectly responsible for more than four times the value of all the money in the world.”

This “robot” directs the actions of the U.S. Federal Reserve, nearly every major bank and Wall Street investment fund and more than 17,000 traders. It also controls half of exchange-traded funds (ETFs), 17% of the bond market, 10% of the stock market and carries out 250,000 trades daily.29

Its powerful artificial intelligence and algorithms are so instrumental that Anthony Malloy, CEO of New York Life Investors, which manages $238 billion in assets, told Forbes, “Aladdin is like oxygen. Without it we wouldn’t be able to function.”30 Even when it comes to government regulation, BlackRock is there.

The U.S. government appointed Brian Christopher Deese as the 13th director of the National Economic Council — he previously worked as the global head of sustainable investing at BlackRock. Adewale Adeyemo, a former BlackRock chief of staff, was also appointed as a top official at the Treasury Department.31 “This means BlackRock is now the treasury as well as the treasury adviser,” notes futurist and social entrepreneur Roger James Hamilton.32

Humans Are Free also explained,33 “Bloomberg calls BlackRock ‘The fourth branch of government,’ because it’s the only private agency that closely works with the central banks. BlackRock lends money to the central bank but it’s also the adviser. It also develops the software the central bank uses.”

In 2019, Blackrock expanded Aladdin’s reach even further by acquiring eFront, a private markets data firm, to gain a “whole portfolio view.”34 This put the private assets that were once a blind spot for Aladdin firmly under its thumb — including data on the global real estate market, data that BlackRock used to buy up single-family homes in the coming years.

“I’m not into conspiracy theories, but even a skeptic with eyes wide open can see the signs. We’re at a point where no one can compete without Aladdin,” Hamilton said, adding:35

“This story is far from over. Aladdin has already reached a tipping point where one robot controls more wealth than any person or country. But as Aladdin’s AI capabilities continue to grow, and with its rate of control rising by another trillion to $2 trillion in new assets every year, it looks inevitable that Wall Street’s secret weapon could end up owning everything, and we end up owning nothing.”

- 1, 3, 4, 5 Fortune June 26, 2022

- 2 CNN April 13, 2022

- 6 Yahoo! June 26, 2022

- 7 Joint Center for Housing Studies of Harvard University, The State of the Nation’s Housing 2022, June 22, 2022

- 8 The State of the Nation’s Housing 2022, Page 2

- 9 The State of the Nation’s Housing 2022, Page 12

- 10 ZeroHedge June 22, 2021

- 11, 12, 14, 15 Housing Wire September 1, 2020

- 13 Housing Wire November 22, 2019

- 16 Reuters June 22, 2021

- 17 Yahoo Finance June 22, 2017

- 18 Slate June 19, 2021

- 19 YouTube June 10, 2021

- 20, 21 The Wall Street Journal April 4, 2021

- 22, 23 World Economic Forum, BlackRock

- 24 Bitcoin.com, News June 11, 2021

- 25 Cultural Husbandry Twitter June 11, 2022

- 26 Forbes November 10, 2016

- 27 YouTube, This Robot Already Owns Everything: Blackrock Aladdin November 29, 2021, 0:20

- 28 The New Statesman April 6, 2018

- 29 YouTube, This Robot Already Owns Everything: Blackrock Aladdin November 29, 2021, 0:40

- 30 Forbes December 19, 2017

- 31 YouTube, This Robot Already Owns Everything: Blackrock Aladdin November 29, 2021, 6:58

- 32 YouTube, This Robot Already Owns Everything: Blackrock Aladdin November 29, 2021, 7:12

- 33 Humans Are Free May 5, 2021

- 34 Institutional Investor May 20, 2020

- 35 YouTube, This Robot Already Owns Everything: Blackrock Aladdin November 29, 2021, 6:45